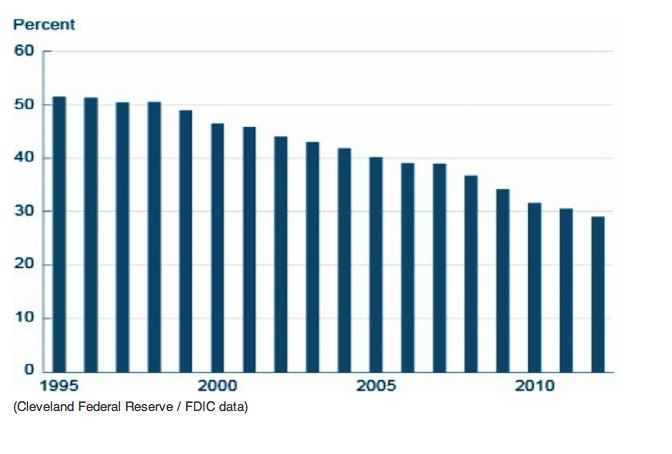

It doesn’t appear that the recession is what caused the small business lending slowdown. It appears the decline in flow of money to Main Street started long before 2008. “Cleveland Federal Reserve analysts published the paper last week, which indicates that the flow of loans to small companies remains very slow and is not likely to pick up anytime soon,” writes J.D. Harrison for the Washington Post. “In addition, as you can see below, their findings show that the relationship between small firms and banks started to grow cold more than a decade ago, at a time when the economy was still expanding.”

It doesn’t appear that the recession is what caused the small business lending slowdown. It appears the decline in flow of money to Main Street started long before 2008. “Cleveland Federal Reserve analysts published the paper last week, which indicates that the flow of loans to small companies remains very slow and is not likely to pick up anytime soon,” writes J.D. Harrison for the Washington Post. “In addition, as you can see below, their findings show that the relationship between small firms and banks started to grow cold more than a decade ago, at a time when the economy was still expanding.”

Please don’t interpret this as an indictment against banks—it isn’t. In fact, there are a number of highly motivated banks (along with credit unions and non-bank lenders) that work with us at Lendio, who are ready and anxious to provide small business loans to Main Street. Nevertheless, I don’t think we can ignore the fact that traditional lending to small business is in decline and in many cases, small business owners are forced to look into alternatives to the bank to find the financing they need.

Harrison outlines a number of the factors that have contributed to the decline, and they point at small business as well as the bank. He says, “…weak financials from the past few years and declining property values have made it difficult for small business owners who want loans to quality for credit, particularly because banks have heightened their lending standards in the wake of the recession.”

Although many small business owners have discovered they have options to the bank, I still believe a healthy relationship between community banks and local businesses is good for Main Street. I understand that the last few years have been hard on small business owners. Robbing Peter to pay Paul may help a business owner stay afloat, but it can be devastating to his or her credit rating—severely limiting their options at the local bank.

Bankers by nature are risk averse. If you wait until you are in dire straights to approach your local banker, odds are he or she will say “no.” With that in mind, here are a few of the things the bank (or any other lender for that matter) will want to see to make sure you’ll be able to repay a loan.

-

1.Credit Score: This one just isn’t going away. If your credit score is below 650, before you go into the bank you should do some work on the measure every lender will ask about. Of course, some lenders will work with you even if you have a poor credit score, but it comes with a cost. You’ll likely pay higher interest rates and fees. They charge the higher rates because a poor credit history is a red flag that you’re a poor credit risk. If you need help repairing your credit, there are people out there who can help you. In fact, Lendio partners with companies who offer those types of services.

2.Time in Business: It’s no secret the first few years of any company are sketchy. Surviving those early years can be a good indication that you’ll still be in business long enough to pay off a loan. That’s why most bankers are looking for at least four or five years in business. You’ll seldom be able to go into the bank with an idea-stage company (a company that isn’t doing any business yet) and walk out with a loan. Of course there are exceptions. If you have exceptional personal credit and can demonstrate to the bank that you have a plan for loan repayment. Otherwise, I don’t know of a banker willing to roll the dice with your business idea, regardless of how good it sounds. They want to see a healthy credit score and four or five years in business before they’ll even consider it.

3. Annual Revenues: Bankers want to evaluate your ability to repay a loan. If your company has no revenues, or very little, it doesn’t bode well for your ability to repay. Although I understand the desire to acquire cash to ramp up, bankers want to see profits (or at least potential profits) before they’re going to stick their neck out for you and your business.

Over the last couple of years alternative (non-bank) lenders have stepped up with cash for Main Street business owners. And, as more companies enter the field, the cost of this type of financing has come down. However, I question whether Main Street can stay alive unless we reverse the trend of the last nearly 20 years and get the community bankers, who have traditionally been where small business went for financing, back in the action.

There is no silver bullet or magic pill we can take to turn things around. I’m suggesting community banks start looking at additional loan products that might fill the gap between the loans they’re writing now and the small business owner loan requests they’re turning away. There are a number of banks across the country successfully doing this. The SBA needs to make it more attractive for banks to participate in more micro-loans. The Feds need to relax some of the regulations that hamstring banks regarding the types of borrowers and the types of loan products they can offer—I think the risk aversion pendulum has swung to far. And, small business owners need to shoulder some of the burden and take responsibility for their poor financial health.

I’d love to hear from those who’ve had great success with the local bank as well as any banker who is taking an innovative approach to the Main Street lending challenges we all recognize. You can reach out to the TDS Business Blog on Twitter, Facebook or by leaving your comments below. You can also reach out to Ty on Twitter.

No comments yet.